-

. . . even AFL-CIO officials concede what employers have long since held: It's cheaper to pay overtime rather than hire additional employees with the heavy fringe costs that go with each worker.

. . . even AFL-CIO officials concede what employers have long since held: It's cheaper to pay overtime rather than hire additional employees with the heavy fringe costs that go with each worker. - Business Week, January 26, 1963

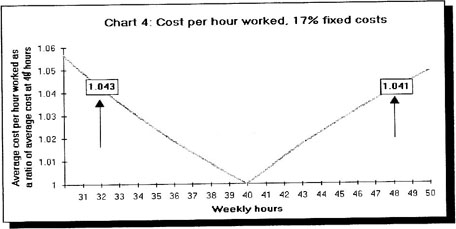

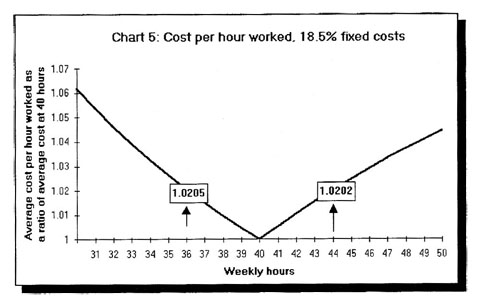

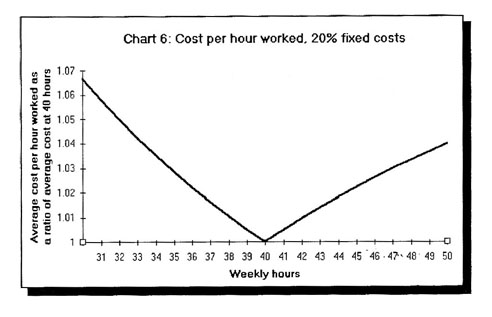

Up to now, this essay has discussed the overtime premium and the factors that diminish its effectiveness as a policy tool for limiting work time. It's bad enough that the limitation of the work time has been bypassed by a loophole and that even the fee for using that loophole has been waived by yet another loophole. But there is yet a further irony: given current structures of compensation, it is often cheaper for employers to increase the hours of work above the legal maximum than it is to reduce work time the same number of hours below that maximum. In keeping with the definition of the overtime premium as a tax, it is appropriate to call the excess cost of reduced work time an undertime tax.

For example, if 17 percent of total labour costs for a 40 hour week are fixed, it is more expensive to reduce work time by eight hours a week than it would be to increase work time by the same number of hours (Chart 4).

Let's review the logic of the argument so far: the overtime premium, while permitting the exceptional use of overtime, was intended to discourage the regular use of overtime. But, the offsetting effect of fixed labour costs undermined the premium as a disincentive for the regular use of overtime. As those fixed labour costs rose above a certain threshold, they became a barrier to the reduction of work time. Because the cost of reducing work time has become greater than the cost of scheduling overtime, adjustments to work time are now more likely to result in overtime than in shorter work time. Not only is the overtime premium ineffective in discouraging regular overtime, it is now producing an effect opposite to its intent.